Betting Against the House

Are modern conveniences gambling with millennials' future?

“The modern economy sells convenience in small payments.

What it quietly replaces is ownership.”

Spend a few minutes listening to the modern housing debate and a familiar conclusion appears almost immediately: millennials cannot afford homes. The American dream, we are told, has become unreachable for an entire generation. The explanation usually follows the same path. Housing prices have risen, student loan debt is high, and wages have not kept up with inflation. Those claims contain some truth. Home prices in many cities did rise dramatically during the past decades, and the Federal Reserve Bank of St. Louis shows that the median home price in the United States moved above $420,000 during the housing surge of the early 2020s.

But when a single explanation becomes widely accepted, it is often worth asking what parts of the story are missing. One question rarely asked in discussions about housing affordability is how spending habits have changed. The modern economy has quietly altered the way people spend money, not through one major event, but through hundreds of small conveniences that encourage people to spend in ways previous generations never could. Each purchase may seem minor on its own. The cumulative effect is what matters.

The Rise of the Convenience Economy

A few decades ago, the typical household had a fairly short list of recurring expenses. There was rent or a mortgage, utilities, a car payment, a phone bill, and maybe cable television. That covered most of it. Today, it is easy for a young adult to accumulate a long list of monthly charges without paying much attention to any of them. Streaming services, music subscriptions, app memberships, cloud storage plans, premium phone services, grocery delivery, ride sharing, and food delivery platforms all become part of the background of everyday life.

None of these expenses appears especially large by itself. Many cost ten or fifteen dollars each month, which is precisely why they are so easy to dismiss. The issue is not the size of each individual charge. The issue is how many of them exist and how easily they pile on top of one another. A 2024 survey from C+R Research found that the average American spends about $273 per month on subscription services alone. Many people underestimate the total because the payments are spread across multiple apps, cards, and billing dates. What feels like a handful of harmless charges can quietly become thousands of dollars over the course of a year.

Food spending tells the same story from a different angle. The Bureau of Labor Statistics reported in 2024 that American households now spend more money eating outside the home than they spend on groceries. Average annual spending on restaurants, takeout, and delivery exceeded $8,200 per household. That was not the case for most of the twentieth century, when families generally spent more on groceries than on restaurants. Cooking at home was normal. Dining out was occasional. Technology changed that balance, and the change was not merely technological. It was behavioral.

Food delivery platforms expanded rapidly during the early 2020s, and by 2025, Americans were spending roughly $95 billion per year on food delivery, according to Statista estimates. A dinner that once required driving across town, parking the car, and waiting in line can now appear at the door after a few taps on a phone. Removing effort from spending tends to increase how often people spend. If a purchase requires real-time and inconvenience, it happens occasionally. If it requires almost no effort at all, it becomes part of the weekly routine.

The Arithmetic of Small Luxuries

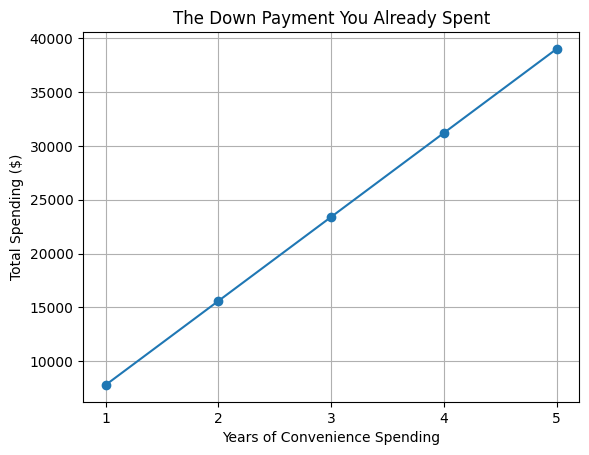

Coffee purchases have become a symbol in many economic debates, and critics often mock the idea that coffee spending has anything to do with financial security. But arithmetic does not depend on symbolism. A typical coffee from Starbucks costs around six dollars. Someone who buys coffee on weekday mornings spends about thirty dollars per week, which becomes roughly $1,560 per year. Over five years that amounts to about $7,800.

Now, most people do not buy coffee every single day, and that is not really the point. Many do buy it several times each week, and the larger issue is the pattern rather than the specific beverage. Repeated convenience purchases create a steady flow of spending that can easily pass unnoticed because each transaction seems too small to matter. But small, repeated expenses have a way of becoming large when measured over years instead of days.

The pattern becomes much clearer when several habits occur at the same time. Imagine a young professional who spends seventy dollars per month on coffee purchases, two hundred dollars on food delivery, three hundred dollars on restaurants during evenings and weekends, and another eighty dollars on streaming subscriptions and other digital services. The combined total approaches $650 each month. That equals roughly $7,800 per year, and over five years, the total reaches about $39,000. That number is interesting for one reason above all others: it is close to what many first-time home buyers need for a down payment and closing costs.

Housing Prices Depend on Location

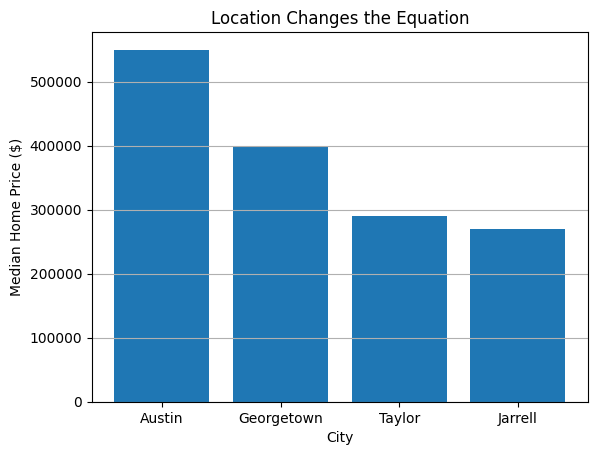

Housing prices do vary widely, and location remains one of the most important variables in the entire discussion. Austin Texas, has experienced enormous population growth during the past decade, and home prices rose accordingly. During the pandemic housing boom, the median price in the Austin area moved above $550,000. Yet housing markets do not stop at the edge of the city, and that fact is often ignored in the broad claim that homeownership is simply unattainable.

Communities such as Georgetown and Temple sit within commuting distance of Austin and offer meaningfully lower home prices. In early 2026, many homes in Temple sold between $260,000 and $330,000 according to regional MLS listings. Georgetown tends to be somewhat higher, but it still remains below the prices found in central Austin. Consider a home priced at $320,000 in one of those areas. A conventional loan with ten percent down would require a $32,000 down payment, and closing costs might add about $7,000. The total cash requirement would therefore be around $39,000.

Now consider income. Pew Research Center estimates that the median millennial household income in the United States is roughly $75,000. After taxes, that income might produce about $4,500 per month in take-home pay. A common spending pattern for someone renting in Austin might look something like this: rent around $1,900, a car payment near $500, groceries about $600, restaurants and delivery around $400, and perhaps another $500 for phone plans, subscriptions, and entertainment. The total approaches $4,300 each month. Under those circumstances, very little money remains available for savings.

What Happens When Spending Changes

This is where the conversation usually becomes uncomfortable, because the numbers begin to show that behavior matters. Small changes in spending habits can alter the timeline significantly. Reducing restaurant spending from four hundred dollars to one hundred saves three hundred dollars each month. Eliminating most delivery orders may save another two hundred. Cutting back on subscriptions and entertainment spending may save an additional one hundred or two hundred dollars. Those adjustments alone approach five hundred dollars per month.

If rent is reduced by sharing housing or choosing a less expensive apartment, savings may increase by another three hundred dollars. Monthly savings can then reach $1,300 to $1,500. Saving $1,400 per month means accumulating $39,000 in about twenty-eight months, which is slightly more than two years. Even allowing for unexpected expenses, the timeline may extend to three years. That is a very different picture from the claim that homeownership is simply impossible.

This does not mean the process is painless. It means the process involves tradeoffs, which is something earlier generations generally understood more clearly. Saving for a first home often meant living with roommates longer, driving an older car, cooking more meals at home, and buying a house that was not in the trendiest neighborhood. Those were not signs of oppression. They were part of the cost of building ownership.

What the Monthly Payment Looks Like

After purchasing the home, the monthly housing cost may not differ dramatically from rent. A $320,000 home with ten percent down leaves a loan of about $288,000. With mortgage rates around 6.5 percent in early 2026, the principal and interest payment would be roughly $1,820 per month. Texas property taxes are relatively high, and in Temple and surrounding areas they often approach 2.2 percent of property value. That adds about $585 per month. Homeowners insurance might cost about $180 per month.

The total monthly housing cost becomes approximately $2,585. That is somewhat higher than many apartment rents, but not dramatically higher. Rent for a comparable apartment in Austin often falls between $1,900 and $2,400. The difference, of course, is that part of the mortgage payment builds equity. If a $320,000 home increases in value by three percent per year, it would be worth roughly $430,000 after ten years. That represents more than $100,000 in additional equity, not including the principal paid down through mortgage payments.

Housing Supply Matters, But So Do Habits

None of this means housing affordability concerns are imaginary. Housing supply has been restricted in many cities for decades through zoning rules and development restrictions. In numerous places, city governments dominated by the Democrat Party have resisted higher-density housing construction. Strict zoning policies often limit the building of apartments, townhouses, and smaller starter homes. Such policies may protect existing homeowners from neighborhood changes, but they also reduce housing supply and increase prices for everyone else.

Housing policy matters, but spending habits matter as well. Earlier generations usually approached their first home differently. The first house was rarely located in the most fashionable neighborhood. It was often smaller and farther from work. People accepted those compromises because the purpose of that first house was not comfort. The purpose was equity.

Modern expectations have shifted. Many people now expect their first home to resemble the homes their parents purchased after twenty years of career progress. When expectations rise faster than incomes, the numbers stop working. Convenience spending encourages the same shift in priorities because it normalizes comfort today rather than security tomorrow.

The Tradeoffs That Remain

The modern economy is very effective at selling convenience. It is far less interested in encouraging delayed gratification. That does not make homeownership impossible. It simply changes the tradeoffs involved. The real question is not whether millennials can afford homes in the abstract. The real question is what they are willing to sacrifice to buy one.

Location can change. Spending habits can change. Timelines can change. When those variables move, the mathematics often moves with them as well. Previous generations built wealth primarily by owning things such as homes, businesses, and investments. Modern life increasingly encourages people to rent nearly everything, from housing and entertainment to transportation and even groceries.

Ownership requires patience and restraint. Convenience requires only a credit card. The long-term results of those two paths are rarely the same.

Help Restore the Habit of Thinking Long Term

Most commentary today is built for outrage, not understanding.

The goal is not to explain how things work. The goal is to win the news cycle, stir emotions, and move on to the next controversy.

But real problems rarely work that way.

Housing, culture, economics, education, and politics are all connected. If people never stop long enough to examine the incentives behind them, the same mistakes repeat themselves over and over.

That is what this publication is trying to change.

Each essay here takes the time to examine the numbers, the history, and the incentives that shape the world around us. The goal is not to follow the daily outrage cycle. The goal is to explain the forces that actually shape our society.

If you believe this kind of work matters, there are several ways to support it.

Become a Paid Subscriber

Paid subscriptions make this work possible.

They allow me to spend the time researching data, examining historical context, and writing essays that go deeper than the typical headline or social media argument.

If you value clear thinking and honest analysis, becoming a paid subscriber is the most direct way to support this work.

Become a paid subscriber:

https://mrchr.is/help

Make a One-Time Gift

Not everyone wants another monthly subscription.

If you prefer, you can support the work with a one-time contribution. Every contribution helps keep the research and writing going.

Support with a one-time gift:

https://mrchr.is/give

Join The Resistance Core

For readers who want to support this mission at the highest level, there is The Resistance Core.

Members of the Resistance Core help sustain the investigative work behind these essays and make it possible to publish consistently.

If you believe this kind of analysis is needed more than ever, joining the Resistance Core is the strongest way to back it.

Join the Resistance Core:

https://mrchr.is/resist

What Your Support Builds Right Now

Your support helps expand the work in several directions:

deeper investigative essays

more data-driven analysis

historical research that challenges popular myths

long-form writing that social media rarely allows

my favorite, keeping me from starving

This kind of work takes time, and time is what your support provides.

If You Cannot Give

You can still help more than you might think.

Simply sharing essays like this with others helps the ideas reach new readers. Word of mouth remains one of the most powerful forces on the internet.

Words of wisdom! "It means the process involves tradeoffs, which is something earlier generations generally understood more clearly. Saving for a first home often meant living with roommates longer, driving an older car, cooking more meals at home, and buying a house that was not in the trendiest neighborhood. Those were not signs of oppression. They were part of the cost of building ownership."

Excellent article Chris. I am 63 so the last of the boomer generation. Every American problem comes down to simply culture. I have a 22-year-old daughter and a 26-year-old daughter. The younger one is a fine girl but I noticed that none of her friends will work. They go to school, they play games, and that’s really about it. Only my daughter amongst that group has a job. They piss and moan about how their lives have no future.

At the same time my neighbor is in his mid 30s and is a plumber. He makes about $200,000 a year and could massively increase that if he could just hire people that would work. There is no way any of my daughter‘s friends are ever going to unplug sewage lines for a living. They were all raised thinking they were special brilliant snowflakes and now they are confronted with the reality that they are average. Which means that half of them are below average. Being average and not very interested in working is that conducive to the American dream.

I’ve been an entrepreneur and been in business for 40 years and I’ve never seen a period where it’s easier to make money and be successful than it is today. But all the tools, let alone the will, to do that seem to be missing from an entire generation.